New: autoweg has been redesigned for an even better selling experienceView news & updates

Full coverage vs. third-party, bonus-malus system, premium comparison and real savings tips. The complete guide to car insurance in Switzerland.

Editorial Team

The autoweg editorial team consists of Swiss automotive market experts creating in-depth guides and market analyses.

Car insurance is the second largest cost of car ownership in Switzerland after the purchase price. Yet most car owners never review their insurance — paying hundreds of francs too much every year.

Swiss car owners spend an average of CHF 1,800 per year on car insurance. Through smart optimization — the right coverage level, optimal deductible and bonus-malus maintenance — you can save up to CHF 1,200 per year without sacrificing essential protection.

In this guide, we show you step by step how to analyze and optimize your car insurance. With real numbers, an interactive savings calculator and experience from over 3,000 car sales on autoweg.

Most Swiss car owners can save CHF 500-1,200 per year by (1) choosing the right coverage level, (2) optimizing the deductible, and (3) comparing providers every 2-3 years.

The bonus-malus system (also claims-free discount) determines your insurance premium based on your claims history. Each claim-free year reduces your premium (bonus), each claim increases it (malus). In Switzerland, levels typically range from 37% (best bonus) to 275% (worst malus) of the base premium.

(44 words)

The biggest mistake is keeping full coverage too long. From a vehicle age of 5-6 years and a value below CHF 15,000, switching to partial coverage almost always pays off.

There are three main types of car insurance in Switzerland. The right choice depends on vehicle age, value and your personal situation.

Covers damage you cause to others. Legally required for every registered vehicle in Switzerland.

Additionally covers theft, glass breakage, natural events, marten damage and animal collisions.

Additionally covers self-inflicted damage to your own vehicle, vandalism and parking damage.

The bonus-malus system has the biggest impact on your premium. Here's how it works:

After 15+ claim-free years. You pay only 37% of the base premium.

New insurance without history. Full base premium.

After multiple claims. Nearly triple the base premium.

Tip: For a small claim (under CHF 2,000), it's often better to pay out of pocket rather than claiming on insurance. A single claim can increase your premium by CHF 300-500/year for 3-5 years.

The timing of the switch is the most important savings tip for car insurance:

When your car's market value drops below CHF 15,000, full coverage is no longer worth it in most cases. The extra premium of CHF 600-1,200/year exceeds the additional protection.

For most new cars, after 4-6 years the market value has dropped enough to make switching to partial coverage sensible. For premium brands (BMW, Audi, Mercedes), it may take 6-8 years.

For leased vehicles, full coverage is typically contractually required. Only after the lease ends can you choose freely.

For vehicles over 25 years old, there are special classic car insurance policies that are significantly cheaper than standard comprehensive coverage.

Many clients are afraid to switch insurers. Yet switching in Switzerland is simple and the bonus-malus transfers 1:1. There's no reason to stay with an expensive provider.

Use these comparison portals to find the best premium:

Largest Swiss comparison service. Compares over 40 insurance offers.

Independent comparison portal focused on value for money.

Quick comparison with quote requests directly from providers.

Compare at least every 2-3 years. Insurers regularly adjust their rates — loyalty is rarely rewarded.

Calculate your personal savings potential

Calculation based on average values. Your actual savings may vary.

These mistakes cost Swiss car owners millions every year

Many keep full coverage even though the vehicle value has long dropped below CHF 15,000. The extra premium far exceeds the additional protection.

Check your vehicle's market value annually and adjust coverage accordingly.

CHF 600-1,200/year

Loyalty is rarely rewarded by insurers. Those who never compare often pay 20-40% more than necessary.

Compare every 2-3 years on comparis.ch or moneyland.ch.

CHF 300-500/year

A CHF 0 deductible costs significantly more than CHF 500 or CHF 1,000 — often CHF 200-400/year more.

Choose a deductible of CHF 500-1,000. The premium savings almost always outweigh the risk.

CHF 200-400/year

Reporting every small scratch to insurance ruins your bonus-malus standing. A reported CHF 500 claim can cost CHF 1,500-2,500 in extra premiums over 3-5 years.

Pay claims under CHF 2,000 yourself — it's cheaper long-term.

CHF 1,500-2,500 over 3-5 years

Roadside assistance, passenger insurance, GAP insurance — many add-ons are redundant or already covered by other insurance (TCS, credit card).

Check each add-on: isn't it already covered elsewhere?

CHF 100-300/year

Total potential excess costs: CHF 2,700-4,900 per year

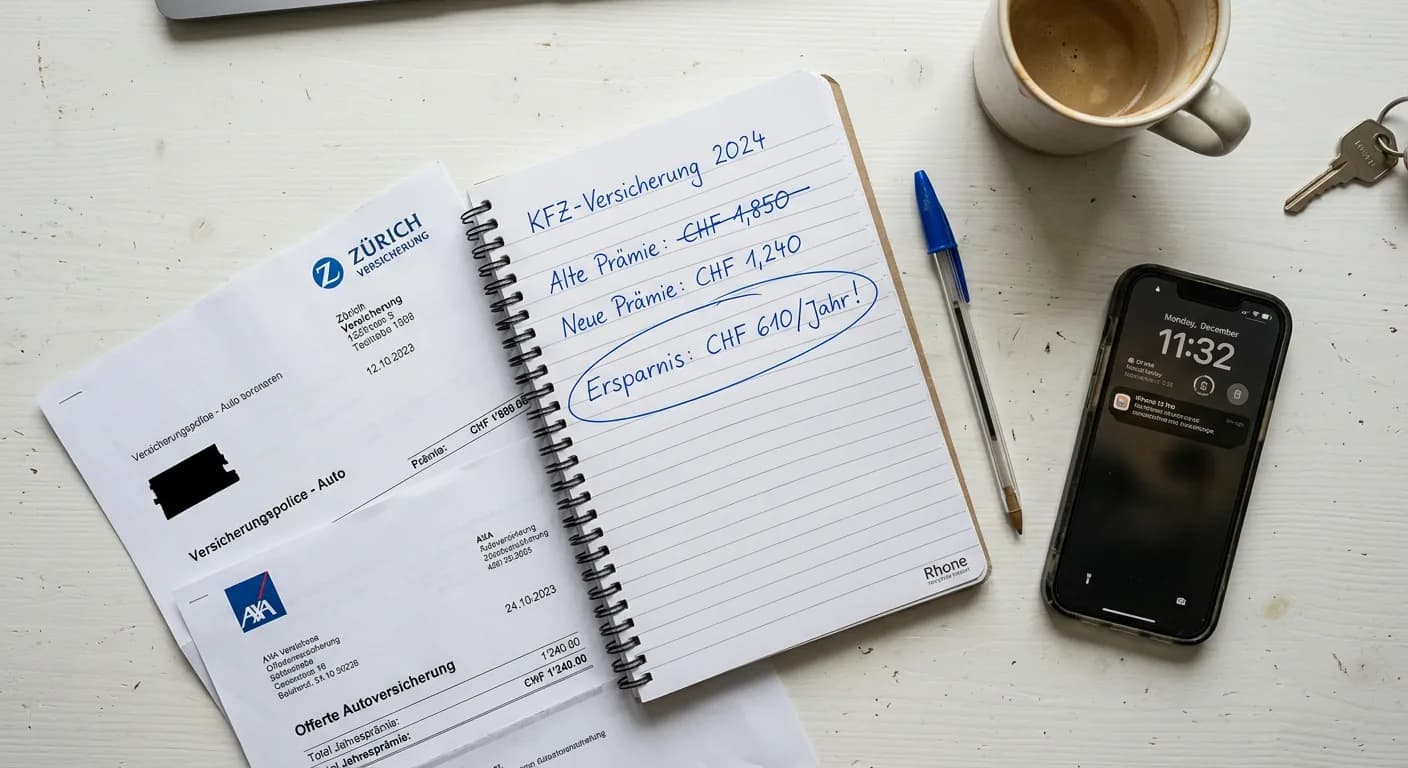

Marco, 35, drives a 7-year-old VW Golf (market value: CHF 12,000). Since purchase, he had full coverage with Mobiliar for CHF 2,340/year with CHF 200 deductible. He had zero claims in 7 years.

Marco compared on comparis.ch, switched to partial coverage with Baloise, increased his deductible to CHF 1,000 and dropped the unnecessary passenger insurance. His bonus-malus transferred 1:1.

Through three simple changes, Marco saves CHF 1,140 per year — without sacrificing essential insurance protection. The switch took 20 minutes online.

At autoweg, we see daily how insurance costs impact total ownership cost. Those who smartly optimize insurance at purchase time often save more over the holding period than on the purchase price.

When I founded autoweg, insurance was one of the most common topics among our clients. Many were selling their car — with no idea how much they could save on insurance. One client was paying CHF 2,800/year full coverage for a 9-year-old Opel Astra worth CHF 6,000.

Since then, we've accompanied over 3,000 car sales and see daily how insurance costs impact total ownership cost. Our advice: review your insurance at least as often as you wash your car. It pays off.

We want every Swiss car owner to know exactly which insurance they need — and which they don't. Transparency saves real money.

Patrick Steiner

Founder, autoweg.ch

Answers to the most important questions about car insurance in Switzerland

Still have questions? Contact us — we're happy to help.

Optimizing car insurance is easier than most people think. In three concrete steps, you can save hundreds of francs per year in less than an hour.

Insurance & Tax

Insurance & TaxWhen and how to cancel your insurance after selling. Calculate your refund, avoid common mistakes, and understand special termination rights.

Read Legal & Documents

Legal & DocumentsStep-by-step guide to deregistering your vehicle at the road traffic office. With checklist, costs and deadlines for all 26 cantons.

Read Legal & Documents

Legal & DocumentsWhat must be in the purchase contract? All important clauses, legal tips and what to watch out for when selling your car.

Read