New: autoweg has been redesigned for an even better selling experienceView news & updates

How I discovered leasing cars are profitable by buying back my VW Polo — and why I founded autoweg.ch

Editorial Team

The autoweg editorial team consists of Swiss automotive market experts creating in-depth guides and market analyses.

Leasing car buyback (leasing arbitrage) is a legal strategy in Switzerland where you buy back your leased vehicle at the end of the contract at residual value and make a profit by reselling it.

In July 2021, I decided to buy back my VW Polo from my leasing company. At that time, I had no idea this decision would lead not just to owning a car, but to founding autoweg.ch. Here's the simple reality: if you know what to look for, leasing returns in Switzerland can be extremely profitable. In this article, I'll show you exactly how it works — using my own story and real numbers from my business.

But let me be honest with you: leasing cars aren't right for everyone, and there are real pitfalls. That's exactly why I wrote this complete guide. You'll learn how to spot real profit opportunities, what legal traps exist, and most importantly: how to use platforms like autoweg.ch to get maximum offers from dealers — something that took me considerable time and effort in 2021.

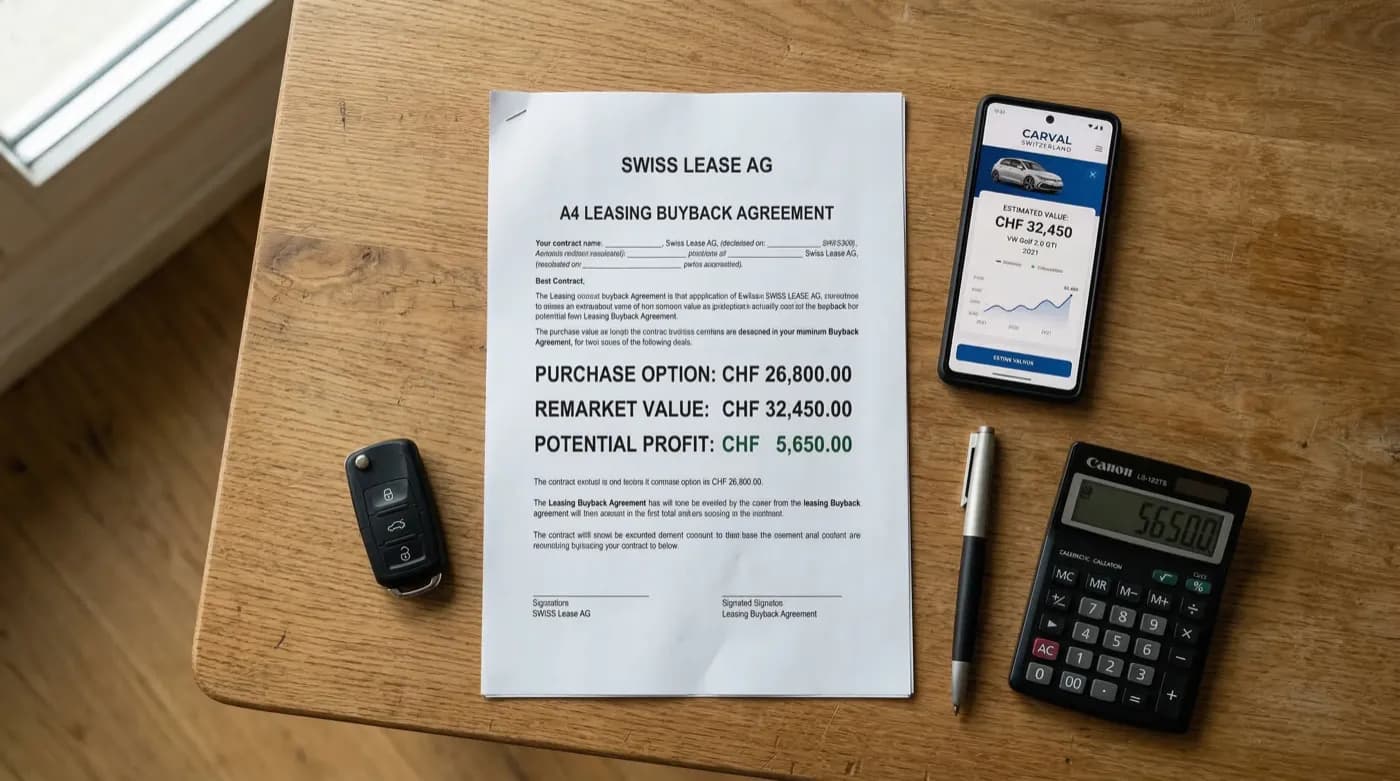

Leasing car buyback is a financial concept where you purchase your leased vehicle at the end of the lease term at the contractually set residual value and then sell it privately. The profit is created when the actual market value exceeds the residual value — in Switzerland, typically by 10–20%. This is completely legal and transparent.

(56 words)

Leasing car buyback is a financial concept where you purchase your leasing vehicle at the end of the leasing term (at the so-called residual value) and then sell it privately. The profit is created when the selling price exceeds the residual value. In Switzerland, this is completely legal and transparent — as long as you know the rules.

Watch out: many leasing contracts contain a hidden clause called 'profit-sharing right'. Some leasing companies have the right to 25% of any profit if you sell at a gain.

The solution: read your leasing contract carefully. Search for the keywords 'right of first refusal', 'profit sharing', 'residual value', 'buyback right'. If you're unsure, ask the leasing company in writing. That's your legal protection.

This was my moment that changed everything. In July 2021, I called AMAG Leasing and said: 'I want to buy back the Polo.' What followed was a journey through the used car market that frustrated me, thrilled me, and turned me into a founder.

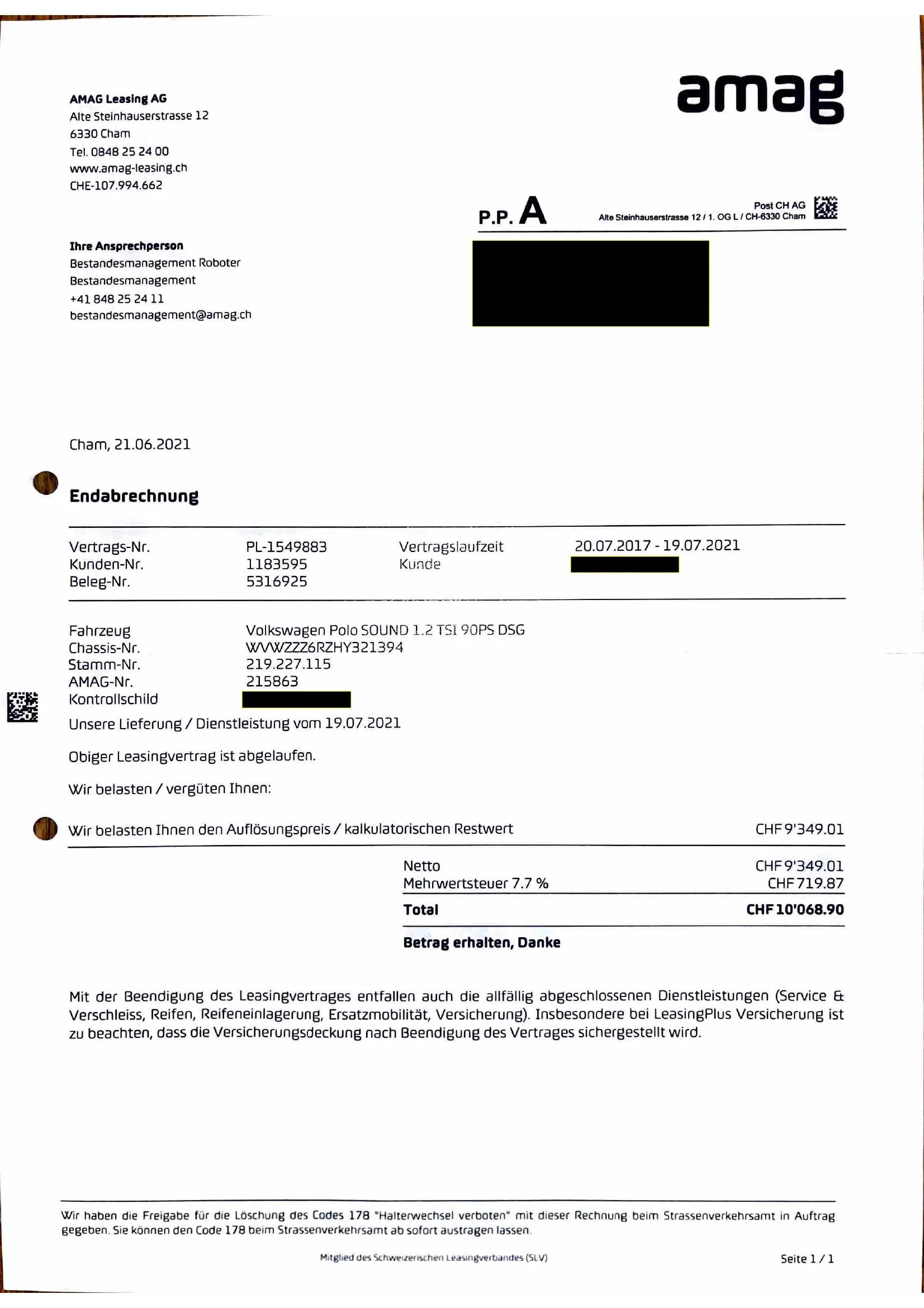

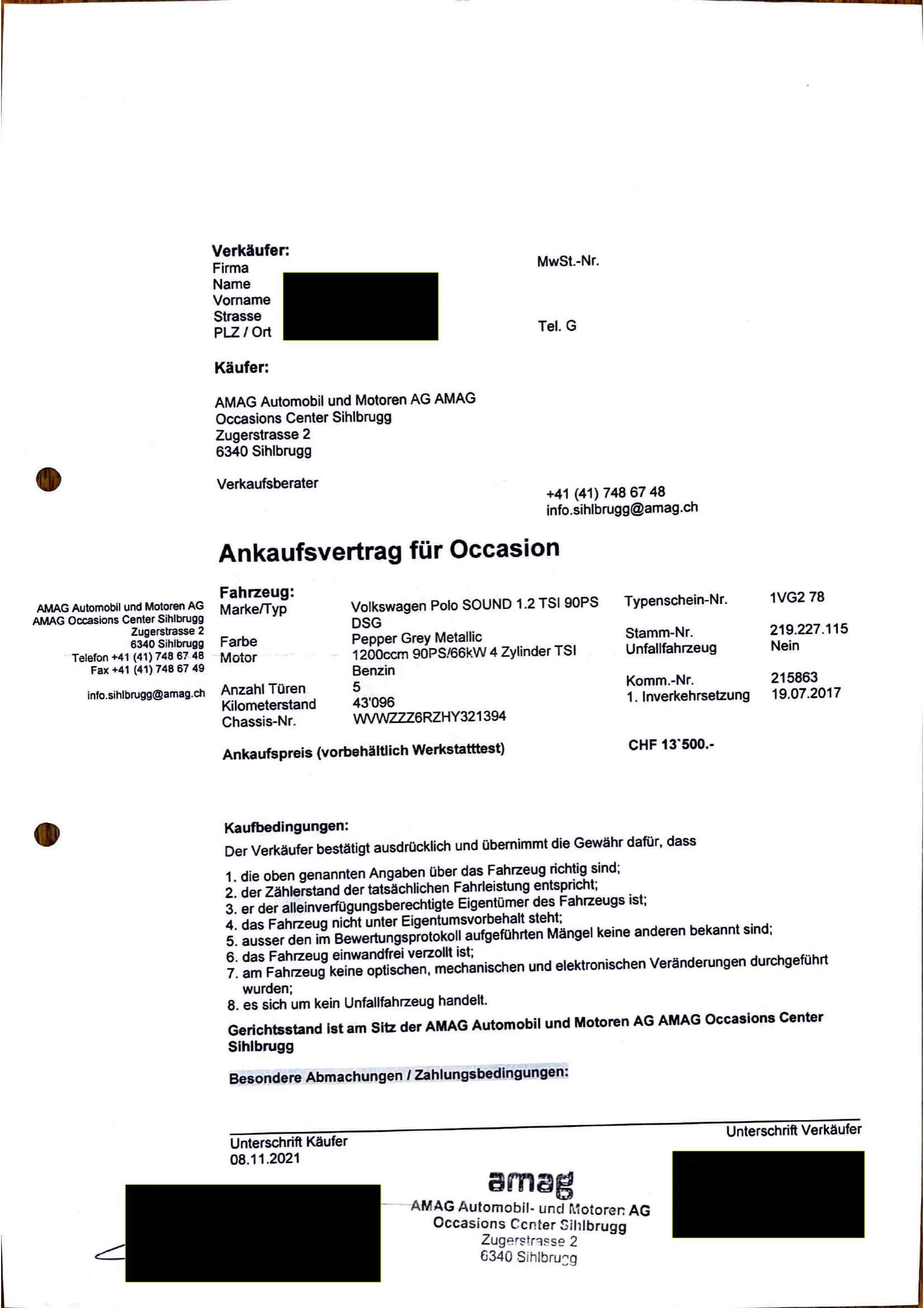

Here are the real documents from my transaction. Personal data has been redacted to protect privacy.

Buyback at calculated residual value: CHF 10,068.90 (incl. VAT)

Sale to AMAG Occasions Center Sihlbrugg: CHF 13,500

Note: All personal data (names, account numbers, vehicle identification numbers, etc.) has been redacted for privacy reasons. The documents are still authentic proof from my real transaction.

Ideally 6–12 months before leasing end

You need three critical pieces of information: (1) The residual value (buyback price), (2) Conditions for buyback, (3) Clauses about right of first refusal or profit sharing

Where to find: In letters from your lessor or online in your customer account (if available)

I read my contract and thought: 'I don't understand a word of this.' That's normal. Just ask. Leasing companies answer such questions routinely.

Auto valuation services like Schwacke (via insurance companies) or TÜV appraisals cost CHF 150–300

Very accurate, but only worthwhile for cars > CHF 15,000

Potential Profit = Market Value – Buyback Price – Additional Costs – Time Value

Notify your leasing company 2–4 months before lease end that you want to buy back

Pay the buyback price + any administrative fees (normally CHF 100–200 together)

The leasing company handles the vehicle handover and inventory record (vehicle registration document)

You register the car in your name. You need: Vehicle registration document, passport, proof of address. This takes ~30 minutes at the local traffic authority

If you can't pay the buyback price in cash, ask your bank about a quick auto loan. Some banks offer special terms for car buybacks. This is cheaper than a regular personal loan.

Advantages:

Disadvantage: It takes 24–48 hours instead of getting a price immediately

Process:

Advantages: You have immediate control and can negotiate personally

Disadvantages: You must Google 10–30 dealers, call them, write emails, and schedule appointments. That takes 20–40 hours. That's the reason I founded autoweg.ch.

Advantage: You reach private buyers who often pay more than dealers

Disadvantage: Many inquiries, long selling time, risk of payment defaults, insurance issues during sales period

Calculate your potential profit from car leasing arbitrage

This tool provides an estimate only. Consult a financial advisor for detailed analysis.

Compare the three main options for selling your bought-back leasing car

| Criterion | Private Sale | Dealer Trade-in | autoweg.ch |

|---|---|---|---|

| Typical Sale Price | Highest (CHF market value) | Lowest (wholesale -10-20%) | High (competitive dealer bids) |

| Time to Sale | 2-8 weeks | Same day | 24-48 hours for offers |

| Effort Required | High (photos, listings, negotiations, viewings) | Low (drive in, get offer) | Low (upload photos, receive offers) |

| Number of Offers | Variable | 1 offer | Multiple (400+ dealers) |

| Scam Risk | Medium-High | None | None (verified dealers) |

| Negotiation Required | Yes, extensive | Limited | No (dealers compete) |

| Best For | Maximum price seekers with time | Quick, hassle-free sale | Best price with minimum effort |

Maximum price, maximum effort

Convenience, lower price

Best balance: high price, low effort

For leasing buyback profits, autoweg.ch offers the optimal balance: competitive dealer prices without the hassle of private selling.

Important: If you realize buyback doesn't make sense, returning at lease end is free and completely fine. There's no guilt involved.

In Switzerland, you have a statutory right to buy back the car at the end of the lease with most leasing contracts. This is regulated under the Swiss Code of Obligations (OR) Article 257, if you have an 'option lease'.

There are two types of leasing: (1) 'Pure Leasing' — you must return it, (2) 'Option Leasing' — you can buy it. My contract was option leasing.

But be careful: the lessor could have a 'right of first refusal'. That means: you must offer it to them first before selling to a third party. That's legal if it's in your contract.

Check your contract: Does it say 'right of first refusal' or 'option leasing'? If yes, respect it. Typically, right of first refusal means: the lessor has 5 days to match the offer. After that, you can sell.

Warning: This is the trickiest point. Some leasing contracts give the lessor the right to take 25% of the profit.

The 'profit-sharing right' is partially enforceable in Switzerland, but there are limits. A blanket right to 25% is problematic because it can be interpreted as 'participation in asset value', which isn't always permitted.

But: There are court rulings saying that 'fair profit sharing' is acceptable if clearly defined in the contract. My contract didn't have it — so I kept 100% of the profit.

Scenario: Your residual value is CHF 10,000, you sell for CHF 13,000, surplus = CHF 3,000.

During leasing: During leasing you pay insurance as the leasee (usually included in the lease or extra).

After buyback: After buyback YOU MUST insure yourself before driving. It's legally required (liability insurance minimum). Insurance costs CHF 40–100/month, depending on the car and your profile.

Taxes: Taxes: profit from the sale isn't automatically income. Whether it's taxable depends on: (1) Is this a 'business activity' or a 'private asset'? (2) Did you hold the car for longer (>1 year)?

Exception: Exception: If you commercially buy and sell multiple cars this way, it could become taxable ('occasional trading').

Important: I recommend consulting a tax professional if your profit is > CHF 5,000. The consultation costs CHF 100–300, but saves you tax stress later.

Not every leasing buyback ends in profit. Here are the real risks.

You buy back the car and sell it for CHF 4,000 profit — but your contract has a 25% profit-sharing clause you missed. The leasing company claims CHF 1,000.

Loss:

CHF 1,000 unexpected cost

Prevention:

Always check your contract for profit-sharing clauses before buyback.

You estimated the market value at CHF 18,000 based on listing prices. But listing prices aren't selling prices — actual dealer offers come in at CHF 15,500, barely above the CHF 15,000 residual value.

Loss:

Near-zero profit after fees

Prevention:

Use real dealer offers (via autoweg.ch), not listing prices. Account for the 10-15% gap between listing and selling price.

After buyback, a detailed inspection reveals underbody rust or previous accident damage not in the service history. Market value drops by CHF 2,000-3,000.

Loss:

CHF 2,000-3,000 in value

Prevention:

Get a pre-purchase inspection (CHF 150-250) BEFORE committing to the buyback.

You buy back the car but forget to arrange insurance immediately. The vehicle sits uninsured for 3 weeks. A parking lot scratch costs CHF 1,500 out of pocket.

Loss:

CHF 1,500+ uninsured damage

Prevention:

Arrange insurance BEFORE the buyback date. Contact your insurer at least 2 weeks in advance.

You find a buyer at CHF 17,000, but the leasing company exercises their pre-emptive right and buys the car at the residual value. You lose the potential profit entirely.

Loss:

Full profit (CHF 2,000-5,000)

Prevention:

Check for pre-emptive right clauses. If present, consider if the risk is worth it. Some lessors rarely exercise this right.

Which Swiss leasing companies allow buyback? What are their profit-sharing rules?

| Provider | Buyback Allowed? | Profit-Sharing Clause | Pre-emptive Right | Notes |

|---|---|---|---|---|

| AMAG Leasing | Yes | Varies by contract | Sometimes | Largest Swiss lessor. Terms vary by dealer agreement. |

| Credit Suisse / UBS Leasing | Yes | Often 25% | Yes, common | Bank-backed leasing. Stricter contract terms. |

| Migros Bank Leasing | Yes | Rarely | No | Generally more favorable terms for buyback. |

| BCGE Leasing | Yes | Varies | Sometimes | Regional (Geneva). Check specific contract. |

| PostFinance Leasing | Yes | Sometimes | Rarely | Straightforward terms. Good for buyback. |

| carvolution | See terms | N/A | N/A | Auto subscription model. Different from traditional leasing. |

| LeasePlan | Yes | Often 25% | Yes | Fleet-focused. Corporate leasing specialist. |

Information based on publicly available contract terms as of 2025. Always verify current terms with your specific leasing provider.

Before signing any leasing contract, ask specifically: (1) Can I buy back the car at the end? (2) Is there a profit-sharing clause? (3) Does the lessor have a pre-emptive right? Get the answers in writing.

That's the mistake I made. I got an offer from AMAG Occasions (CHF 13,500) and was done. Only later did I realize: another dealer might have paid CHF 14,500. I lost that CHF 1,000.

Solution: Always compare at least 5–10 dealers. Use autoweg.ch or call yourself. Each additional inquiry takes 5 minutes — the benefit is CHF 500–2,000.

Many lessees only discover at buyback that a right of first refusal or profit-sharing clause is in the contract. Then it's too late to negotiate.

Solution: Read the contract 6 months before lease end carefully. Ask the leasing company in writing about right of first refusal and profit sharing. Everything in writing is your proof.

If you don't know what the car is worth, you negotiate blind. The first offer price is often CHF 500–1,000 too low.

Solution: Research on autostat.ch, autoscout24.ch, mobile.de at least a week beforehand. Note 5–10 comparable prices. That gives you negotiation confidence.

If you wait until the lease expires (last week), you have no time for market research or negotiation. Dealers know this and pay less.

Solution: Start 3–4 months before lease end. That gives you time to analyze market conditions, request buyback, and plan the sale.

If tax authorities later ask why you 'made a profit', you have no proof of purchase price, buyback price, comparable market offers. That can get expensive.

Solution: Save everything: purchase contract, buyback confirmation, comparable offers, sale invoice. A folder with copies costs nothing but saves you in a dispute.

“The Swiss used car market has consistently shown that leasing residual values are set conservatively. For vehicles in good condition with average mileage, the gap between residual value and actual market value typically ranges from 10-20%.”

“Many leasing customers don't realize they have the option to buy back their vehicle. By simply returning it to the dealer, they leave thousands of francs on the table. Informed consumers who compare offers can capture this value.”

“When comparing multiple dealer offers — rather than accepting the first quote — Swiss car sellers typically achieve 8-15% higher sale prices. This difference can be the margin that makes leasing arbitrage profitable.”

Use this checklist to make sure you don't miss anything in your leasing buyback.

Yes, you must notify the leasing company 2–4 months in advance. Usually there's an order process. Write an email with the words 'I want to buy back the vehicle' + vehicle number + date. That's your proof you notified them in time.

Usually not, if your contract is option leasing. But they can set additional conditions, like 'The car must be in top condition' or 'Service records must be complete'. Check if you've met all conditions.

For me it was 4 months. This depends on: (1) How fast the leasing company is (2–4 weeks), (2) How fast you sell (1–4 weeks with autoweg.ch, weeks–months with private sale).

Yes, you need liability insurance (legally required). Comprehensive insurance is optional. Some insurers offer 'leasing car' rates that are cheaper. Ask your insurer.

That's possible (e.g., older cars, bad markets). Then you have two options: (1) Buy back and sell at a loss (e.g., –CHF 1,000), (2) Simply return the car (costs you CHF 0). Most lessees choose to return it.

Yes, that's the advantage. I drove my Polo for 4 more months after buyback — that saves you rental car costs. The wear and tear until sale is your problem, but it's usually worth it for 2–4 months.

You need: (1) Vehicle registration document (Fahrzeugausweis), (2) Service record (optional, but helpful), (3) Repair receipts (as proof of condition), (4) Insurance policy (for the buyer). With autoweg.ch you only need the basic information — we handle the rest.

Yes, completely legal. There's no hidden regulation forbidding it. But: Respect your contract terms (profit sharing, right of first refusal). As long as you respect your contract, you're safe.

Leasing car buyback is NOT the quick path to wealth. It's a solid opportunity when the numbers work.

I earned CHF 3,431 because I analyzed the numbers. But I could have earned CHF 4,200 if I'd compared 10 dealers instead of 1. That's my biggest mistake — and the reason autoweg.ch exists today. You'll do better.

Leasing Guides

Leasing GuidesLearn about the garage's right of first refusal when buying back a leased car. Which providers enforce it, and how to navigate it.

Read Leasing Guides

Leasing GuidesUnderstanding profit-sharing clauses in Swiss leasing contracts. How they work, which providers enforce them, and strategies to minimise their impact.

Read Leasing Guides

Leasing GuidesCompare all options at the end of a Swiss lease: return, buyback, or renewal. Decision framework with calculation examples.

Read